The Internal Revenue Service taxes different kinds of income at different rates. Some types of capital gains, such as profits from the sale of a stock that you have held for a long time, are generally taxed at a more favorable rate than your salary or interest income. However, not all capital gains are treated equally. The tax rate can vary dramatically between short-term and long-term gains. Understanding the capital gains tax rate is an important step for most investors.

Automatically import investment transactions from hundreds of financial partners and maximize your rental property deductions with TurboTax Premier. It’s free to start, and enjoy $15 off TurboTax Premier when you file.

What is a capital gain?

Capital gains are profits you make from selling an asset. Typical assets include businesses, land, cars, boats, and stocks. When you sell one of these assets for more than the price you paid to buy the asset, that can trigger a taxable event. This often requires that the capital gain on that asset be reported to the IRS on your income taxes.

What’s the difference between a short-term and long-term capital gain?

Generally, capital gains are taxed according to how long you’ve held a particular asset – known as the holding period. Profits you make from selling assets you’ve held for a year or less are called short-term capital gains. Alternatively, gains from assets you’ve held for longer than a year are known as long-term capital gains. Typically, there are specific rules and different tax rates applied to short-term and long-term capital gains. In general, you will pay less in taxes on long-term capital gains than you will on short-term capital gains.

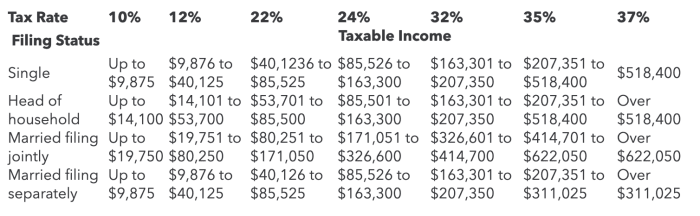

What is the 2020 short-term capital gains tax rate?

You typically do not benefit from any special tax rate on short-term capital gains. Instead, these profits are usually taxed at the same rate as your ordinary income. This tax rate is based on your income and filing status. Other items to note about short-term capital gains:

- The holding period begins ticking from the day after you acquire the asset, up to and including the day you sell it.

- For 2020, ordinary tax rates range from 10% to 37%, depending on your income and filing status.

2020 Short-Term Capital Gains Tax Rates

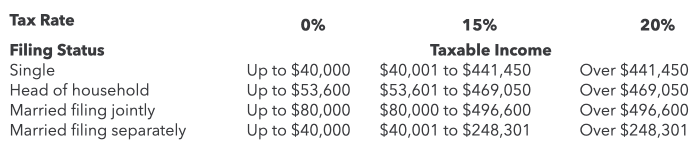

What is the 2020 long-term capital gains tax rate?

If you hold your assets for longer than a year, you can often benefit from a reduced tax rate on your profits. Those in the lower tax bracket could pay nothing for their capital gains rate, while high-income taxpayers could save as much as 17% off the ordinary income rate, according to the IRS.

2020 Long-Term Capital Gains Tax Rates

What are the exceptions to the capital gains tax rate for long-term gains?

One major exception to a reduced long-term capital gains rate applies to collectible assets, such as antiques, fine art, coins, or even valuable vintages of wine. Typically, any profits from the sale of these collectibles will be taxed at 28% regardless of how long you have held the item.

Another major exception comes from the Net Investment Income Tax (NIIT), which adds a 3.8% surtax to certain net investments of individuals, estates, and trusts above a set threshold. Typically, this surtax applies to those with high incomes who also have a significant amount of capital gains from investment, interest, and dividend income.

Don’t worry about knowing tax rules. With TurboTax Live, you can connect with real tax experts or CPAs to help with your taxes — or even do them for you. Get unlimited tax advice right on your screen from live tax experts as you do your taxes, or have everything done for you—start to finish. So you can increase your tax knowledge and understanding and be 100% confident your return is done right, guaranteed.

What is the capital gains rate for retirement accounts?

One of the many benefits of IRAs and other retirement accounts is that you can defer paying taxes on capital gains. Whether you generate a short-term or long-term gain in your IRA, you don’t have to pay any tax until you take money out of the account.

The negative side is that all contributions and earnings you withdraw from a taxable IRA or other taxable retirement accounts, even profits from long-term capital gains, are typically taxed as ordinary income. So, while retirement accounts offer tax deferral, they do not benefit from lower long-term capital gains rates.

How can capital losses affect your taxes?

As previously mentioned, different tax rates apply to short-term and long-term gains. However, if your investments end up losing money rather than generating gains, those losses can affect your taxes as well. However, in this case, you can use those losses to reduce your taxes. The IRS allows you to match up your gains and losses for any given year to determine your net capital gain or loss.

- If after fully reducing your gains with your losses and you end up with a net loss, you can use up to $3,000 of it per year to reduce your other taxable income.

- Any additional losses can be carried forward into future years to offset either capital gains and up to $3,000 per year in ordinary income.

- Since you don’t generate capital gains or losses in a retirement account, you can’t use losses in IRAs or 401(k) plans to offset gains or your other income.

How can you minimize capital gains taxes?

There are several ways you can minimize the taxes you pay on capital gains:

- Wait to sell assets. If you can keep an asset for more than a year before selling, this can usually result in paying a lower capital gains rate on that profit.

- Invest in tax-free or tax-deferred accounts. By investing money in 401(k) plans, Roth IRA accounts, and 529 college savings plans, you could save significantly in taxes. This is because these investments are able to grow tax-free or tax-deferred, meaning that you won’t have to pay capital gains taxes on any earnings right away — and in certain circumstances, you won’t pay any tax even when you take the money out.

- Don’t sell your home too quickly. One major exception to the capital gains tax rate on real estate profits is your principal residence. If you have owned your home and used it as your main residence for at least two of the five years prior to selling it, then you can usually exclude up to $250,000 of capital gains on this type of real estate if you’re single, and up to $500,000 if you’re married and filing jointly. It’s also important to note that you typically can’t exclude multiple home sales from capital gains taxes within two years.

Whether you have stock, bonds, ETFs, cryptocurrency, rental property income or other investments, TurboTax Premier is designed for you. Increase your tax knowledge and understanding all while doing your taxes.

This article is auto-generated by Algorithm Source: www.thestreet.com